Dharma DeFi stands at the forefront of a rapidly evolving decentralized finance landscape. As investors seek reliable ways to generate yields amid market volatility, platforms like Dharma DeFi are drawing attention for their innovative approaches to lending and liquidity provision. This article explores how Dharma DeFi is enabling high-yield opportunities while addressing the challenges of risk management in decentralized lending.

Dharma DeFi 2026: Unlocking High-Yield Opportunities in Decentralized Lending

Dharma DeFi 2026

Decentralized Finance (DeFi) Market Size & Share Analysis – 2025 …

In 2026, Dharma DeFi stands at the forefront of a rapidly evolving decentralized finance landscape. As investors seek reliable ways to generate yields amid market volatility, platforms like Dharma DeFi are drawing attention for their innovative approaches to lending and liquidity provision. This article explores how Dharma DeFi is enabling high-yield opportunities while addressing the challenges of risk management in decentralized lending.

The Rise of Decentralized Lending in a Maturing Market

Decentralized lending has transformed from a niche experiment into a cornerstone of the crypto economy. At its core, it allows users to borrow and lend digital assets without intermediaries like banks. Protocols facilitate this through smart contracts on blockchains, ensuring transparency and efficiency.

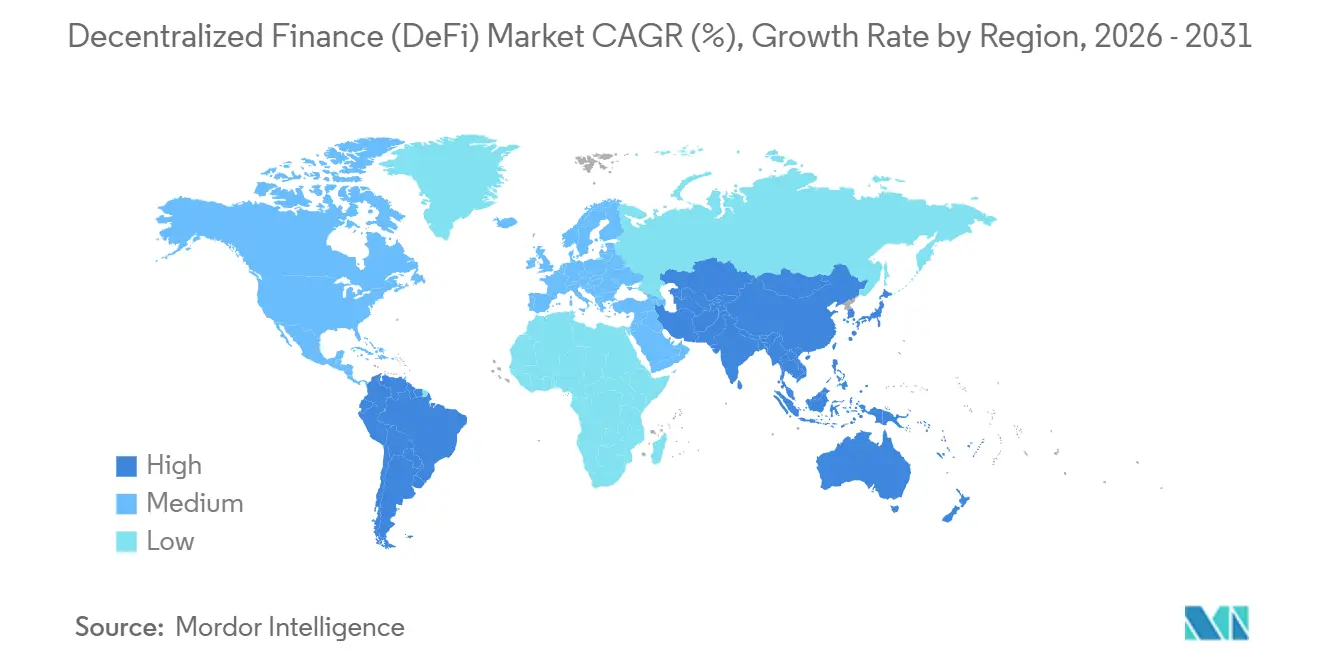

Dharma DeFi, particularly through developments like Velar’s Dharma AMM, exemplifies this shift. Launched to unlock liquidity on Bitcoin, it integrates automated market makers with lending features, allowing users to earn yields on otherwise idle assets. This innovation comes at a time when the overall DeFi market is projected to grow from $42.56 billion in 2025 to $60.73 billion in 2026, reflecting a compound annual growth rate that underscores sustained investor interest.

What drives this growth? For one, the integration of real-world assets into DeFi platforms. Tokenized treasuries and other financial instruments are now commonplace, offering stable yields around 4-5% that rival traditional savings accounts. Yet, as markets mature, the focus shifts from speculative gains to sustainable returns.

Consider a simple analogy: Traditional banking is like a locked vault where your money sits dormant. Decentralized lending, powered by Dharma DeFi protocols, turns that vault into a dynamic engine, where assets work continuously to generate interest.

Innovative Protocols Fueling Dharma DeFi’s Growth

Dharma DeFi’s lending protocols build on foundational DeFi mechanics but introduce enhancements for scalability and accessibility. For instance, peer-to-peer lending models, once popularized by early iterations of Dharma, now evolve with cross-chain capabilities. Users can lend USDC or other stablecoins directly, earning competitive rates while minimizing counterparty risks through over-collateralization.

A key feature is the use of automated market makers (AMMs) in lending pools. In Velar’s Dharma AMM, token pairs trade on-chain, providing liquidity that supports borrowing activities. This setup not only boosts yields but also reduces fees compared to centralized exchanges. In 2026, with Bitcoin DeFi gaining traction, such protocols enable seamless asset movement without wrappers, addressing fragmentation issues that plagued earlier systems.

Moreover, Dharma DeFi leverages oracles to ensure accurate pricing. Without reliable data feeds, lending protocols risk under-collateralized loans leading to liquidations. This is where Chainlink’s oracles play a pivotal role.

Chainlink’s Oracles: Enabling Real-World Data for Altcoin Smart Contracts

Chainlink oracles bridge the gap between blockchains and external data sources, making them indispensable for DeFi lending. In smart contracts, oracles provide real-time price feeds, interest rates, and other metrics essential for risk assessment.

For altcoin-based lending, Chainlink ensures that volatile assets like ETH or SOL are valued accurately against stablecoins. This prevents manipulation and supports features like flash loans, where borrowers access funds instantly for arbitrage opportunities, repaying in the same transaction.

In the context of Dharma DeFi, oracles enable dynamic yield adjustments based on market conditions. For example, if Bitcoin’s price surges, oracle data triggers recalibrations in lending pools to maintain stability. Chainlink’s decentralized network aggregates data from multiple providers, reducing single points of failure and enhancing security.

This integration is crucial as DeFi expands into real-world applications. Prediction markets and tokenized assets rely on oracles for settlement, with Chainlink securing over $137 billion in DeFi value. It’s like having a trusted referee in a game where rules are enforced automatically.

Current Trends Shaping Dharma DeFi and DeFi Lending

The DeFi sector in 2026 emphasizes sustainability over hype. Total value locked (TVL) in lending protocols has risen steadily, with outstanding loans increasing 37.2% year-to-date. This growth aligns with stablecoin market cap expansion, now exceeding $300 billion, as users seek low-volatility options for yields.

Search interest in related terms has surged dramatically. For instance, queries for “onchain” have increased fivefold since early 2024, reaching all-time highs. While specific data on Dharma DeFi shows niche interest, the broader Bitcoin DeFi narrative, including protocols like Dharma AMM, reflects this momentum. Social discussions on platforms like X highlight how these tools simplify asset flows, attracting mainstream investors.

Another trend: The convergence of TradFi and DeFi. Institutional players are tokenizing assets, projecting DeFi’s expansion beyond current boundaries. Dharma DeFi benefits here, offering high-yield opportunities on Bitcoin, a network traditionally underutilized for lending.

Understanding Flash Loans And DeFi Lending

Pros, Risks, and Common Misconceptions in Decentralized Lending

The advantages of Dharma DeFi are clear. High yields—often 4-8% on stablecoins—outpace traditional finance. Accessibility is another plus; anyone with a wallet can participate, democratizing investment. Protocols like Dharma AMM reduce silos, enabling efficient liquidity provision.

However, risks persist. Volatility can trigger liquidations if collateral values drop sharply. Smart contract vulnerabilities, though mitigated by audits, remain a concern. Over-reliance on oracles introduces oracle failure risks, where inaccurate data leads to unfair outcomes.

A common misconception is that DeFi is “risk-free” due to decentralization. In reality, it’s pseudonymous and requires due diligence. Another myth: All yields are sustainable. Many stem from emissions, which can dilute value over time. True real yields, from fees and funding rates, are preferable for long-term strategies.

Strategies for Maximizing Yields While Managing Risks

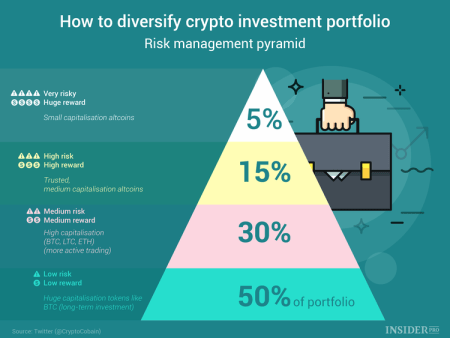

To thrive in Dharma DeFi lending, start with diversification. Allocate across stablecoins, LSTs (liquid staking tokens), and RWAs for balanced exposure. For example, stake in protocols offering 6-7% on SOL or ETH derivatives.

Monitor oracle health; Chainlink’s feeds provide transparency, so verify data sources. Use tools like leverage looping cautiously—borrow against collateral to amplify yields, but maintain healthy loan-to-value ratios to avoid liquidations.

Watch market indicators. In 2026, focus on trends like unified stablecoin layers and privacy enhancements. Engage with communities on X for real-time insights into protocol updates.

Finally, prioritize security. Use hardware wallets and audit protocols before committing funds. This approach turns high-yield opportunities into calculated plays.

A Long-Term Perspective on Dharma DeFi’s Role in Finance

As DeFi matures, Dharma DeFi represents a bridge to inclusive finance. By unlocking yields on underutilized networks like Bitcoin, it reshapes how everyday investors engage with crypto. With oracles like Chainlink ensuring reliability, the ecosystem is poised for deeper integration with traditional systems.

Yet, success hinges on adaptation. Sustainable models will prevail, rewarding patient participants over speculators.

What if decentralized lending becomes the default for global finance—how prepared are you to adapt?

Top Ten References Used for This Article

- https://www.financemagnates.com/thought-leadership/velar-launches-dharma-amm-to-unlock-defi-liquidity-on-bitcoin

- https://www.thebusinessresearchcompany.com/report/decentralized-finance-global-market-report

- https://chain.link/use-cases/defi

- https://www.galaxy.com/insights/research/chainlink-oracle-ccip-price-feeds

- https://www.theblock.co/post/383120/2026-defi-outlook

- https://www.weforum.org/stories/2026/01/digital-economy-inflection-point-what-to-expect-for-digital-assets-in-2026

- https://www.theblock.co/post/306736/google-search-volume-for-onchain-is-hitting-unprecedented-heights

- https://finance.yahoo.com/news/top-defi-trends-watch-2026-060000080.html

- https://www.linkedin.com/posts/norbertgehrke_blockchain-price-oracles-accuracy-and-violation-activity-7392892715572654080-9DL3

- https://onekey.so/blog/learn/oracles-the-backbone-securing-137-billion-in-defi

Note: This is not financial advice. Crypto is volatile; always DYOR and only invest what you can afford to lose.

Read More