In an era where data breaches plague the financial sector, the Decentralized Identifier emerges as a pivotal innovation for safeguarding personal information. As we navigate 2026, with blockchain adoption accelerating and regulatory frameworks evolving, this technology promises to reshape how individuals manage their fiscal identities.

Decentralized Identifier: The Key to Secure Financial Identities in a Digital World

Decentralized Identifier

In an era where data breaches plague the financial sector, the Decentralized Identifier emerges as a pivotal innovation for safeguarding personal information. As we navigate 2026, with blockchain adoption accelerating and regulatory frameworks evolving, this technology promises to reshape how individuals manage their fiscal identities. Traditional systems, reliant on centralized databases, have proven vulnerable, exposing millions to risks like identity theft. However, Decentralized Identifiers offer a path to self-sovereign control, enhancing privacy in personal finance and cross-border transactions. This shift matters now more than ever, as global economies grapple with digital threats.

Consider the stark reality. In 2025, the average cost of a data breach globally stood at $4.44 million, marking a slight decline from previous years but still underscoring the immense financial toll. Financial institutions bore a disproportionate burden, accounting for a significant portion of these incidents. Yet, amid this chaos, blockchain-based solutions like Decentralized Identifiers are gaining traction, empowering users to verify identities without handing over excessive data.

Understanding Decentralized Identifiers

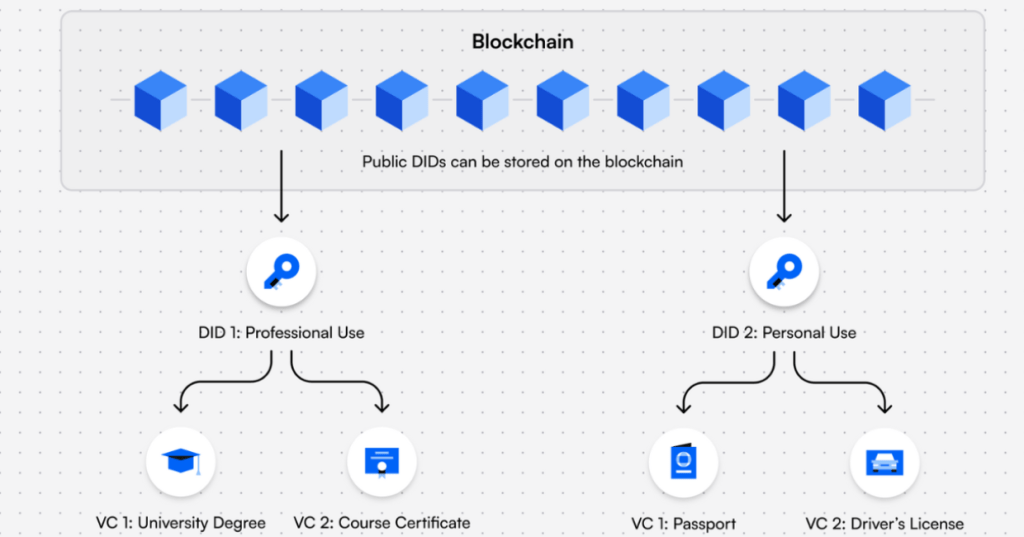

At its core, a Decentralized Identifier (DID) is a unique, verifiable string that represents an entity—be it a person, organization, or even a device—without relying on a central authority. Unlike traditional IDs issued by governments or banks, which store data in silos prone to hacks, DIDs leverage blockchain technology for distribution and verification. This means your identity isn’t locked in one place; it’s portable and under your control.

To illustrate, think of a Decentralized Identifier as a digital passport you own outright. It uses cryptographic keys to prove attributes—like age or creditworthiness—without revealing unnecessary details. For instance, when applying for a loan, you could share just enough information to satisfy requirements, keeping the rest private. Standards like those from the World Wide Web Consortium (W3C) define DIDs, ensuring interoperability across platforms.

How do they work? A DID document, stored on a blockchain, contains public keys, service endpoints, and verification methods. When interacting online, you present verifiable credentials tied to your DID, which others can check against the blockchain. This process eliminates intermediaries, reducing points of failure. In finance, this translates to seamless, secure interactions.

Decentralized Identifiers (DIDs): The Ultimate Beginner’s Guide 2025

The Mechanics Behind Decentralized Identifiers

Diving deeper, Decentralized Identifiers operate through a combination of blockchain ledgers and cryptographic protocols. Users generate a DID via a wallet app, registering it on a compatible network like Ethereum or specialized identity chains. The associated DID document acts as a metadata hub, not storing personal data but pointing to where proofs can be verified.

For example, in a cross-border payment, a Decentralized Identifier allows instant confirmation of sender legitimacy without exposing full banking history. This efficiency stems from zero-knowledge proofs, where you prove a fact (e.g., “I am over 18”) without disclosing the underlying data. Such mechanisms are already integral to projects like SelfKey, which integrates DIDs for compliant DeFi access.

Moreover, DIDs align with self-sovereign identity (SSI) principles, emphasizing user consent and portability. As adoption grows, standards evolve to support diverse use cases, from KYC in banking to credential sharing in fintech apps.

Current Trends in Decentralized Identifier Adoption

Entering 2026, Decentralized Identifiers are at the forefront of blockchain’s maturation. Regulatory shifts, such as the U.S. GENIUS Act mandating stablecoin frameworks by mid-year, are pushing for clearer guidelines on digital identities. Globally, the EU’s eIDAS 2.0 framework encourages SSI models, fostering cross-border interoperability.

In crypto, Ethereum serves as a testing ground for DID integrations, with enterprises exploring proof-of-personhood systems to combat sybil attacks. Tokenization trends amplify this; assets like real estate or stocks are being digitized, requiring robust identity layers to ensure trust. For instance, platforms like Ondo Finance use DIDs to verify participants in tokenized stock pools, blending TradFi with DeFi.

Recent data highlights momentum. Blockchain adoption in finance surged in 2025, with institutional involvement up significantly, as seen in Bitcoin’s price stability amid regulatory clarity. X posts from industry leaders, like those from GLEIF, underscore how verified identities bridge traditional and decentralized finance.

Meanwhile, projects like MEMO lead with DID-focused tokenization, enabling secure data ownership. These trends signal a shift toward scalable, privacy-centric systems.

DeFi Takes on Bigger Role in Money Laundering – Chainalysis

Benefits of Decentralized Identifiers for Financial Security

Decentralized Identifiers shine in bolstering security, particularly by minimizing data breaches in banking. Centralized systems, like those hit in the Capital One breach affecting 100 million users, highlight vulnerabilities. DIDs disperse control, making mass compromises harder.

One key benefit is enhanced privacy. Users share only pertinent data, reducing exposure. In personal finance, this means apps like wallets can verify eligibility for services without full profiles. For cross-border transactions, DIDs streamline compliance, cutting costs and delays—vital as remittances hit record highs.

In DeFi, applications abound. Platforms like Aave could integrate DIDs for undercollateralized lending, verifying credit via off-chain oracles without central oversight. This fosters inclusion, allowing unbanked individuals to participate securely.

Furthermore, DIDs combat fraud. By tying identities to verifiable claims, they deter money laundering, as noted in Treasury assessments. Overall, they promote a resilient ecosystem.

8 Best Data Science Use Cases in Finance | PixelPlex

Real-World Applications in DeFi and Beyond

Decentralized Identifiers are already transforming DeFi. Take Togggle, which uses DIDs to enhance platform security and compliance. Users prove attributes like residency for regulatory adherence, enabling global access without privacy trade-offs.

In fintech, XRP Ledger incorporates DIDs for verifiable identities, facilitating instant settlements. Cross-border examples include remittances via platforms like Wada, where DIDs ensure trust in peer-to-peer transfers.

Looking ahead, 2026 sees DIDs in tokenized assets. Banks like those partnering with Amina explore DeFi pools with identity verification, bridging gaps. This integration accelerates adoption, as evidenced by rising DeFi TVL.

Potential Risks and Common Misconceptions

Despite advantages, Decentralized Identifiers carry risks. One concern is user responsibility; losing private keys could mean permanent identity loss, unlike centralized recovery options. Additionally, blockchain vulnerabilities, like smart contract bugs, pose threats.

Misconceptions abound. Some view DIDs as fully anonymous, but they’re pseudonymous—traceable if linked to real-world data. Regulatory gaps in 2026 could lead to misuse, as surveillance concerns rise. Another myth: DIDs eliminate all breaches. While reducing them, human errors persist.

Privacy risks include data correlation across chains, potentially enabling tracking. Balancing innovation with safeguards is crucial.

Most cyber breaches in financial services and healthcare

Addressing Misconceptions About Decentralized Identifiers

Often, people confuse DIDs with complete decentralization, overlooking hybrid models needed for compliance. In reality, they complement regulations, not evade them. For instance, KYT (Know Your Transaction) tools integrate with DIDs for anti-illicit finance.

Another fallacy: They’re only for crypto experts. User-friendly wallets make implementation accessible.

Actionable Insights for Implementing Self-Sovereign Identities

To adopt Decentralized Identifiers, start with education. Explore wallets like those from Dock or SelfKey for creating DIDs. Follow SSI principles: Ensure control, access, and portability.

Watch trends like EU digital wallets or U.S. stablecoin rules. For investors, monitor projects like Billions Network, emphasizing DID sovereignty. Do: Back up keys securely, use multi-factor verification.

Think long-term: Integrate DIDs into daily finance for privacy gains.

Conclusion: A Long-Term Perspective on Decentralized Identifiers

As 2026 unfolds, Decentralized Identifiers stand poised to redefine financial identities, fostering a secure, inclusive digital world. By addressing vulnerabilities and embracing blockchain, they pave the way for sustainable innovation. Yet, success hinges on balanced regulation and user adoption.

Will Decentralized Identifiers become the standard for your financial interactions, or will traditional systems hold sway?

For a dynamic view of blockchain trends, consider this Bitcoin chart from TradingView: Bitcoin USD Chart, showing adoption growth.

References Used for This Article

- 5 emerging digital ID trends in 2026 that could redefine your online … – http://www.mountainadvocate.com/premium/stacker/stories/5-emerging-digital-id-trends-in-2026-that-could-redefine-your-online-persona,54899

- Crypto heads into 2026 with privacy, decentralized identity on the line – https://www.msn.com/en-us/news/technology/crypto-heads-into-2026-with-privacy-decentralized-identity-on-the-line/ar-AA1SZ2Aw

- Decentralized Identifiers: The Future of Digital Identity – Lightspark – https://www.lightspark.com/glossary/decentralized-identifier-

- 2026 Crypto Outlook – Trakx – https://trakx.io/resources/insights/2026-crypto-outlook

- Decentralized Identifiers (DIDs) v1.1 – W3C – https://www.w3.org/TR/did-1.1

- The 2026 Crypto Landscape: What to Expect and How MEMO is At … – https://blog.memolabs.org/the-2026-crypto-landscape-what-to-expect-and-how-memo-is-at-the-forefront

- Why 2026 Could Be Crypto’s Most Important Year Yet – AMINA Bank – https://aminagroup.com/research/why-2026-could-be-cryptos-most-important-year-yet

- 14 Biggest Data Breaches in Finance – UpGuard – https://www.upguard.com/blog/biggest-data-breaches-financial-services

- 110+ of the Latest Data Breach Statistics to Know for 2026 & Beyond – https://secureframe.com/blog/data-breach-statistics

- Best Decentralized Identity (DID) Projects to Watch in 2024 – KuCoin – https://www.kucoin.com/learn/web3/five-best-decentralized-identity-did-projects

(Note: This is not financial advice. Crypto is volatile; always DYOR and only invest what you can afford to lose.)

Read More